Given the weaker Swedish krona exchange rate it cannot be ruled out that certain suppliers take this competitive edge for granted, delaying innovations.

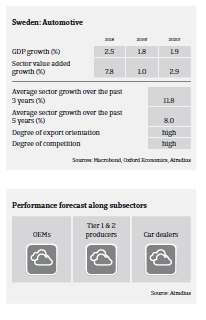

- The Swedish car producer segment is dominated by Volvo Cars in the passenger car segment and by Volvo AB and Scania AB in the truck segment. Those companies are mainly export-oriented (the export ratio amounts to more than 85%) and largely determine the performance of smaller Swedish suppliers. Automotive exports account for about 12% of Sweden´s GDP. Demand from the EU has weakened since the end of 2018 and in 2019 is expected to remain lower than in previous years.

- Due to its high export dependency the automotive sector is exposed to currency exchange risk, as most costs incurred are in Swedish krona. Currently the relative weakness of the Swedish currency still supports international competitiveness.

- Profit margins in the automotive industry have been rather high over the past two years, but are expected to deteriorate slightly in the coming 12 months. Most businesses should be financially resilient enough to cope with volatility in demand or commodity prices. The current interest rate environment (the Swedish benchmark interest rate remains at -0.25%) favours companies in servicing their debt, and banks are willing to lend.

- Depending on the level in the supply chain, payment duration in the automotive sector ranges from 30 to 90 days. The level of non-payments and insolvencies has been low over the last two years. We expect a slight increase in payment delays and insolvencies (up about 2%) in the coming 12 months, mainly triggered by the overall economic slowdown in Sweden and the EU.

- For the time being we do not expect that the credit risk situation of suppliers will seriously deteriorate in the coming 2-3 years due to the industry challenges ahead (shift to e-mobility, pressure from OEMs etc.). Most local suppliers produce high-quality parts, for which there will still be substantial demand in the future. At the same time the lion´s share of the industry is active in the commercial vehicle segment (trucks and buses), where the pressure to swiftly convert to e-mobility is currently still lower than in the passenger cars segment.

- However, given the currently weaker Swedish krona exchange rate it cannot be ruled out that certain suppliers take this competitive edge for granted, delaying innovations/investing in new technology and/or neglecting cost prudency.

- For the time being. our underwriting stance remains generally open to neutral for this industry, with no major restrictions on any subsectors.

Downloads

Market Monitor Automotive 2019

1.19MB PDF