Despite further sales growth most businesses continue to operate on very tight margins due to fierce competition, while equity strength is below average.

- Rising insolvencies and fraud issues impact the sector

- Fierce competition and price pressure

- On average, payments take between 30 and 60 days

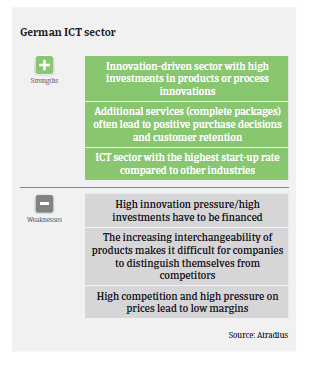

ICT plays a pivotal role in the German economy, outperforming traditional industrial sectors (such as mechanical engineering or chemicals) in terms of innovation and mid-term growth rates. While the German ICT market is dominated by a few big groups, it is characterised by a high number of small- and mid-sized businesses. The sector employs more than one million people, and has generated about 150,000 new jobs over the past five years. 40,000 new jobs are expected to be added in 2019 (up 3.5% compared to 2018), and ICT will remain an engine of employment growth in the long term.

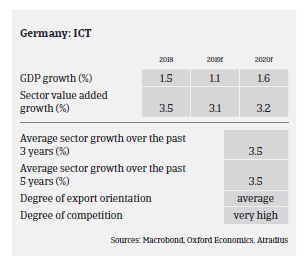

According to the German Federal Association for Information Technology, Telecommunications and New Media (BITKOM), ICT sales increased 2.0% in 2018, to EUR 160.0 billion. This trend is expected to continue in 2019, with a 1.5% growth rate forecast.

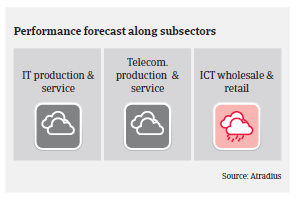

Turnover in the telecommunications segments is back on an upward trend (up 1.6% in 2018 and forecast to grow 1.1% in 2019), while IT sales (IT hardware, software and services) are forecast to increase 2.5% this year. Within this segment, software sales (up 6.3%) are expected to be the main driver of growth - as in previous years. That said the negative trend in consumer electronic sales will continue (5% decline forecast for 2019).

Despite further sales growth, most ICT businesses continue to operate on very tight margins due to fierce competition in all subsectors, while equity strength is below average. High competition and sharp price erosion have led to an ongoing trend of consolidation. Unless they are well-established in niche products, small ICT companies with annual sales below EUR 50 million are – and will continue to be – the losers in this cut-throat environment.

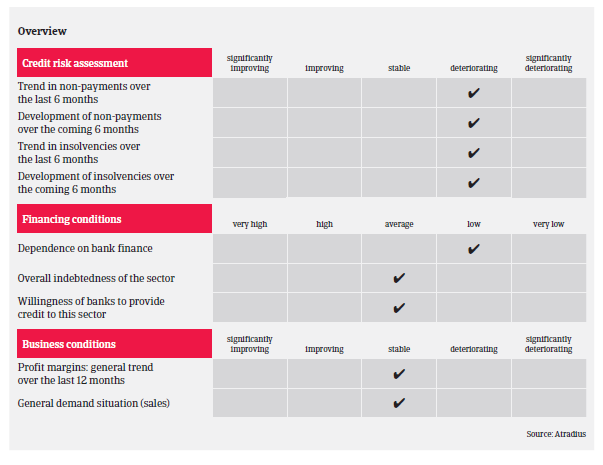

On average, payments in the ICT industry take between 30 and 60 days, in some cases up to 90 days. Due to the more difficult market conditions (fierce competition and price wars), payment delays, insolvencies and credit insurance claims increased in 2018 (according to the latest data available, ICT business failures increased 3.6% year-on-year in H1 of 2018). We expect this negative trend to continue, with a further rise in payment delays and business failures in 2019, especially among smaller ICT companies and in the ICT wholesale/retail segment.

Another issue is that, due to fast changing technology in this industry and low margins, the wholesale and retail of electronic appliances segment is especially susceptible to fraud. We are still particularly cautious about this, as even innocent businesses caught up in a so-called “VAT carousel” can be left bearing significant tax liabilities. This can lead to liquidity issues, “freezing” of accounts by tax authorities and losing sales to customers that are cautious about buying from prosecuted suppliers.

In general, our underwriting approach for the ICT industry is neutral for IT and telecommunications producers and service providers, but more restrictive for ICT wholesalers and retailers, due to the issues mentioned above and the fact that credit insurance claims have increased over recent months. As ICT is a very fast and innovative industry with sharp price erosion and high competition, we require comprehensive information (e.g. interim figures, cash budgets, overview of bank lines, etc.) on each company we underwrite.

Downloads

1.13MB PDF