In both countries there are star players within the sector, while some segments are weaker, e.g. in German beverage subsector profit margins decrease.

European football championship 2016

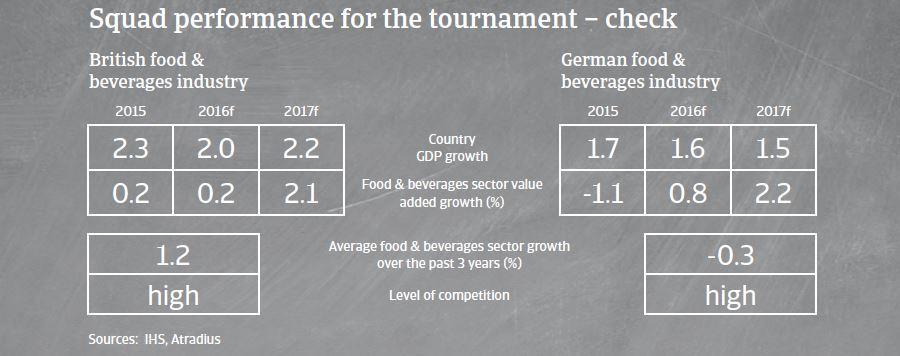

Sector playing field: food industry

Northern Ireland: ambitious growth targets

Food is Northern Ireland’s biggest manufacturing industry, with sales totalling more than GBP 4.5 billion and as many as 100,000 jobs supported by the agri-food sector including farming, fishing, retail and distribution. There are over 400 food and drink processing companies located in Northern Ireland. Meat and dairy are the largest sectors, accounting for about 50% of turnover.

In 2013 the Northern Irish Agri-Food Strategy Board launched an ambitious growth strategy. They have targeted a 60% (from 2010) increase in turnover to GDP 7 billion by 2020.

Northern Irish food businesses profit margins are expected to remain stable in 2016, and banks are willing to provide loans to the industry.

Germany: overwhelming market power of large retailers and discounters

According to the German Food Association BVE, nominal turnover decreased 3.4% in 2015, to EUR 166 billion. While domestic sales decreased 5.7%, export sales just fell 0.1%. Despite decreasing sales, the equity strength of businesses remains good in this sector, but larger groups and producers are usually better capitalised than wholesalers or retailers.

The overwhelming market power of large retailers and discounters and the tough competition and price wars in the food retail sector indicate that food producers, processors and suppliers have found it difficult to pass on costs. As a result, their profit margins have decreased in recent years and are continuing to decline.

Nevertheless, despite the problems in the industry, many companies in all food subsectors are doing well. The food sector is non-cyclical, and thus less volatile than other industries. Moreover, the sector’s export share has almost doubled since the mid-1990s, providing business opportunities abroad.

Players to watch

Northern Ireland

In the beverages industry the main products are soft drinks, beer, whiskey, tea and coffee. While there are approximately 40 companies in the sector, it is driven by three large companies which account for almost 85% of turnover and two-thirds of employment. There is strength from their maturity as organisations, sophistication in their processes, and financial resilience.

The beef and sheep meat sector is the largest sector of the Northern Ireland Agri-Food industry by turnover. The sector relies heavily on external markets with 72% of sales made to businesses outside of Northern Ireland. Its strengths are the quality of livestock and processors equipped with well invested and accredited facilities.

In the dairy segment, the value of milk output decreased 27% in 2015. The volatility in the average milk price over recent years is a reflection of Northern Ireland’s dependence on global commodity markets.

Germany

Meat/meat products is by far the largest subsector, controlled mainly by a few market-leading meat processors who, over recent years, have created fully vertically integrated groups. The rising demand for meat worldwide has provided business opportunities for the German meat industry, with a boost to the profit margins of those with the largest export share.

Despite an expected sales upturn this summer, sales prices in the German beverage industry (beer, mineral water, soft drinks, etc.) remain under pressure because of lower consumption, increasing consumer price sensitivity, overcapacity and discounting. Profit margins continue to shrink in this segment.

Major strengths and weaknesses

Northern Irish food industry: strengths

German food industry: strengths

- Part of the UK, which is a net importer of food

- Reputation as a supplier of wholesome food with the provenance that comes from the values of the local farming industry

- As part of an island, Northern Ireland has a number of distinct advantages for the production of safe food

- Non-cyclical industry

- Innovative industry sector, reacting on changing consumer behaviour

- Profits from increasing export business

- Internationally very competitive

Northern Irish food industry: weaknesses

German food industry: weaknesses

- Farm incomes in Northern Ireland fell steeply in 2015.

- Issues with the potential dual identity of Northern and Irish food products – i.e. both British and Irish

- Partial overcapacities

- Shrinking margins

- Declining number of consumers and ageing society

- Low price levels due to strong discount sector

Fair play ranking: payment behaviour and insolvencies

Northern Irish food industry

The average payment duration in the UK food industry is 45-60 days.

Payment experience has been good over the past two years and protracted payments are low.

Non-payment notifications are low, and we do not expect increases in the coming months.

The level of food insolvencies is low. No insolvency increases are expected in 2016.

German food industry

Food producers and wholesalers pay, on average, within 30 days while payment terms of food retailers often vary between 45 and even 90 or more days

With food processing companies and retailers demanding longer payment terms from their immediate suppliers to improve their working capital, a wave of longer payment terms is being created along the whole supply chain. Still, the already low profit margins are decreasing further.

We have not seen any increase in the number of notified non-payments in the last couple of months and do not expect this in the near future.

Due to the still strong economic environment in Germany, food insolvencies have not increased recently. However, in the medium term the number of defaults could rise, especially for smaller businesses and those with poor financial strength.