A modest increase in payment delays cannot be ruled out in the coming 12 months, but no substantial insolvency increase is expected for the industry.

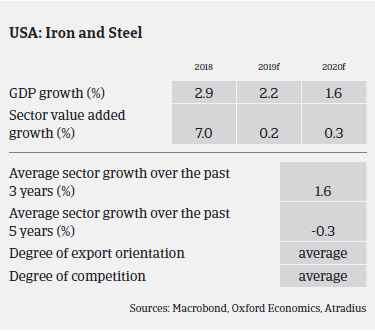

According to the World Steel Association, US steel production increased 3.2% in the period January-September 2019. US metals and steel businesses have benefited from tax cuts on corporations, which allowed companies to improve their infrastructure.

Immediately after the imposition of import tariffs on steel and aluminium by Washington in spring 2018, US metals and steel producers recorded increased revenues and improved profitability (domestically produced steel and metals being less expensive than imported products). The original worry that that many (smaller) steel/metals trading or processing businesses in the US could not pass on higher prices to customers/end buyers has not materialised.

While profits remained steady in H1 of 2019, a decrease is expected in the coming 12 months due to a combination of lower pricing (e.g. steel prices have decreased to pre-tariff levels again) and higher commodity costs, especially for iron ore. At the same time, demand for metals and steel is expected to slow down in 2020, in line with lower economic growth. Automotive production is expected to decrease as a significant amount of 2019 inventory remains on hand. Construction activity has been steady in 2019, with residential building supported by lower mortgage interest rates. However, in 2020 construction activity is due to level off at best.

Payments in the US metals and steel industries take about 60 days on average, and payment experience has been good over the past two years. After the imposition of tariffs payment terms were extended while the market adapted to the changed buying and selling practices. Due to decreasing profits and increased volatility of demand a modest increase in payment delays cannot be ruled out in the coming 12 months. However, no substantial insolvency increase is expected, as even smaller players, thus far, are able to cope with higher prices for tariff-related products.

Our underwriting stance for the steel and metals sector remains generally neutral for all major metals and steel segments. Each buyer must be reviewed on a stand-alone basis. We seek a clear understanding of each buyer’s domestic/international revenue split and the dynamics of their supply chain.

Downloads

1.06MB PDF